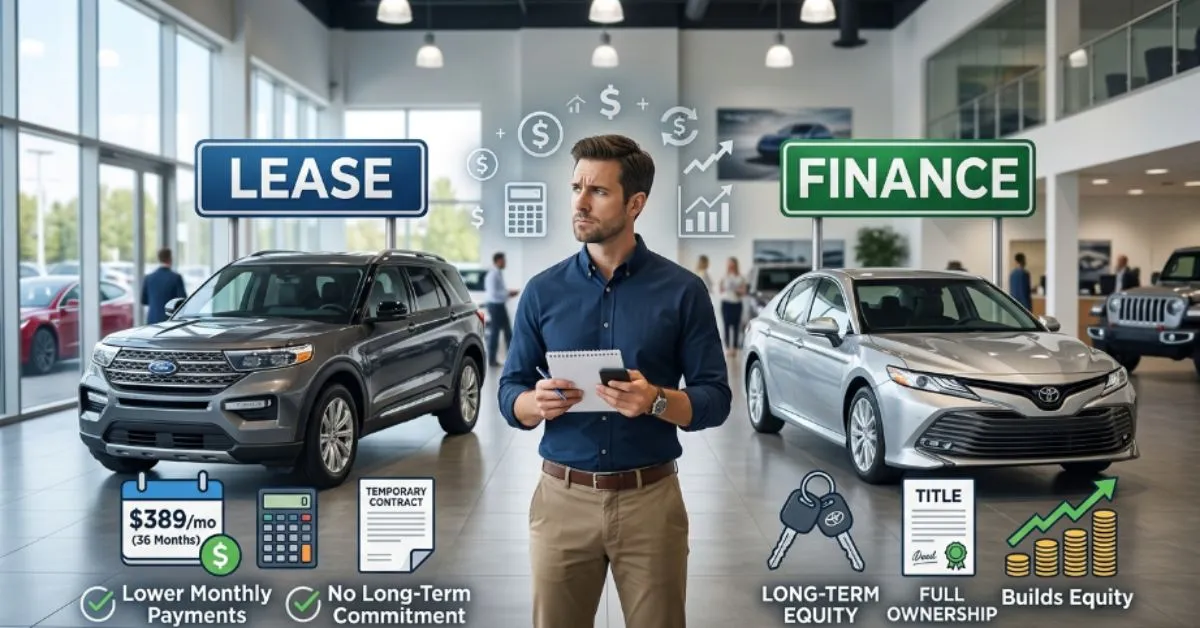

I still remember standing in a dealership, excited about getting a new car. Everything seemed simple until the salesperson asked a question that completely changed the conversation: “Would you like to lease or finance?”

At first, I thought they were basically the same thing. After all, both options let you drive the car home. But the more I looked into it, the more confusing it became. One option offered lower monthly payments. The other promised ownership and long term value. Friends gave different advice, online reviews contradicted each other, and I wasn’t sure which choice would save me more money.

If you’ve ever found yourself comparing lease or finance options, you’re not alone. Thousands of Americans face this decision every year when buying a new vehicle. The choice affects your monthly budget, long term costs, driving flexibility, and even your future financial plans.

The good news is that the difference is much simpler than many people think. In this guide, I’ll break down everything you need to know so you can confidently decide whether leasing or financing is the better option for your situation.

⚡Lease or Finance – Quick Answer

The main difference is simple:

- Leasing means you’re paying to use a vehicle for a specific period, usually 2–4 years.

- Financing means you’re paying to eventually own the vehicle.

Quick examples:

- Want lower monthly payments and a new car every few years? Lease.

- Want to build ownership and keep the vehicle long term? Finance.

- Drive a lot of miles every year? Finance is usually better.

Simple takeaway: If ownership matters, finance. If lower short term costs matter, lease.

🤔 Why Do People Compare Lease or Finance?

Many people compare lease or finance because both options allow them to drive a vehicle without paying the full purchase price upfront.

The confusion happens because:

- Both require monthly payments.

- Both may require a down payment.

- Both involve credit approval.

- Both allow you to drive the same vehicle.

A common assumption is that leasing is always cheaper. While monthly payments are often lower, total costs and long term value can tell a different story.

Another misconception is that financing is always expensive. In reality, financing can become more affordable over time because payments eventually end while ownership remains.

📜 The Background Behind Both Options

Vehicle financing has been around for decades. It became popular as cars became more expensive and consumers needed manageable payment plans. Financing allows buyers to spread costs over several years while gradually building ownership.

Leasing became more popular in the late 20th century. Manufacturers realized many consumers preferred driving newer vehicles regularly instead of keeping one car for many years. Leasing offered lower monthly payments and easier vehicle upgrades.

Today, both options remain popular because they serve different needs. Financing focuses on ownership, while leasing focuses on access and flexibility.

📊 Key Differences at a Glance

| Feature | Lease | Finance |

| Main Purpose | Temporary use | Ownership |

| Monthly Payments | Usually lower | Usually higher |

| Ownership | No | Yes |

| Mileage Limits | Usually yes | No |

| Vehicle Modifications | Limited | Allowed |

| End of Term | Return vehicle | Keep vehicle |

| Long Term Value | Limited | Builds equity |

| Maintenance Costs | Often lower initially | Can increase with age |

| Flexibility | Easy upgrades | Long term commitment |

| Best For | Frequent upgrades | Long term ownership |

Feature by Feature Comparison 🔍

Monthly Payments

Leasing typically offers lower monthly payments because you’re only paying for the vehicle’s depreciation during the lease term.

Financing payments are often higher because you’re paying toward full ownership.

Ownership

This is the biggest difference.

With financing, every payment moves you closer to owning the vehicle outright.

With leasing, ownership stays with the leasing company.

Mileage Restrictions

Most leases include annual mileage limits.

Going over these limits can result in additional charges.

Financed vehicles have no mileage restrictions.

Vehicle Customization

Want custom wheels, modifications, or upgrades?

Financing gives you more freedom.

Leased vehicles often have restrictions because the vehicle must be returned in acceptable condition.

Long Term Costs

Financing may cost more monthly, but ownership can provide value for years after the loan is paid off.

Leasing may cost less each month but can become more expensive if repeated continuously over many years.

Vehicle Condition Requirements

Leased vehicles are inspected when returned.

Excessive wear and tear may lead to extra charges.

Financed vehicles don’t have return inspections because you own them.

Pricing and Value Comparison 💰

Costs vary based on:

- Vehicle price

- Credit score

- Interest rates

- Lease incentives

- Down payment amount

- Loan length

Generally:

Leasing

- Lower monthly payments

- Smaller down payments in some cases

- Potential fees for excess mileage

- Potential wear and tear charges

Financing

- Higher monthly payments

- Interest charges

- Long term ownership value

- No return fees

Remember that prices and financing rates can change over time depending on market conditions and lender policies.

For short term affordability, leasing often wins.

For long term value, financing usually wins.

Pros and Cons ✅❌

Leasing Pros

- Lower monthly payments

- New vehicle every few years

- Often covered by warranty

- Lower repair costs initially

- Easier access to newer technology

Leasing Cons

- No ownership

- Mileage limits

- Wear and tear fees

- Endless payments if continually leasing

- Modification restrictions

Financing Pros

- Full ownership eventually

- No mileage restrictions

- Build equity

- Freedom to customize

- No vehicle return requirements

Financing Cons

- Higher monthly payments

- Larger long term maintenance costs

- Vehicle depreciation affects resale value

- Longer financial commitment

Who Should Choose Leasing? 🎯

Leasing may be ideal if you:

- ✔ Like driving new vehicles every few years

- ✔ Prefer lower monthly payments

- ✔ Drive average or low annual mileage

- ✔ Want the latest safety features

- ✔ Prefer warranty coverage

- ✔ Don’t care about ownership

Example:

A professional who drives 10,000 miles annually and enjoys upgrading vehicles frequently may benefit from leasing.

Who Should Choose Financing? 🎯

Financing may be ideal if you:

- ✔ Want vehicle ownership

- ✔ Plan to keep the car long term

- ✔ Drive many miles annually

- ✔ Want customization freedom

- ✔ Prefer building long term value

- ✔ Don’t want mileage restrictions

Example:

A family planning to keep a vehicle for 8–10 years often benefits more from financing.

❌ Common Mistakes People Make

Mistake #1: Looking Only at Monthly Payments

Lower payments don’t always mean lower overall costs.

Mistake #2: Ignoring Mileage Limits

Excess mileage fees can add up quickly.

Mistake #3: Assuming Ownership Doesn’t Matter

Ownership can create long term financial advantages.

Mistake #4: Not Reading Lease Terms

Some buyers overlook penalties and restrictions.

Mistake #5: Choosing Based on Friends’ Advice

The best option depends on your personal needs, not someone else’s experience.

📝 Real Life Examples

Everyday Situations

A commuter who drives 25,000 miles annually often finds financing more practical.

A city resident who drives occasionally may enjoy leasing benefits.

Social Media Discussions

Many car enthusiasts on social platforms favor leasing because they enjoy changing vehicles frequently.

Others strongly support financing because they dislike permanent monthly payments.

Consumer Reviews

Lease users often praise affordability and convenience.

Finance users often highlight ownership and long term savings.

Professional Discussions

Financial advisors frequently recommend evaluating total cost of ownership rather than monthly payment alone.

Family Decisions

Families often choose financing because they intend to keep vehicles for many years.

🤔 Things to Consider Before Choosing

Budget

Can you comfortably afford higher monthly payments?

Long Term Value

Do you want an asset after payments end?

Driving Habits

Do you exceed typical mileage limits?

Vehicle Preferences

Do you enjoy upgrading frequently?

Personal Goals

Is flexibility more important than ownership?

Maintenance Expectations

How long do you plan to keep the vehicle?

Answering these questions can quickly point you toward the better option.

📋 Quick Comparison Table

| Category | Winner |

| Lower Monthly Payment | Lease |

| Long Term Value | Finance |

| Ownership | Finance |

| Vehicle Flexibility | Finance |

| Easy Upgrades | Lease |

| Best for Beginners | Lease |

| Best for Heavy Drivers | Finance |

| Best Overall Value | Finance |

| Best Convenience | Lease |

| Overall Recommendation | Depends on goals |

FAQs❓

Q. Is leasing cheaper than financing?

Usually monthly payments are lower, but long term costs may not be.

Q. Can I buy a leased car later?

Yes, many leases include a purchase option.

Q. Does leasing hurt my credit?

No, if payments are made on time.

Q. Which option is better for business owners?

It depends on tax situations and vehicle usage.

Q. Is financing better for long term savings?

In many cases, yes, because ownership creates lasting value.

Q. Are maintenance costs lower with leasing?

Often yes, since leased vehicles are usually newer and under warranty.

Q. What happens when a lease ends?

You typically return the vehicle, buy it, or start another lease.

Q. Can I trade in a financed vehicle?

Yes, many dealerships accept trade ins.

Q. Is leasing good for first time car buyers?

It can be if lower monthly payments are a priority.

Q. Which option is best for high mileage drivers?

Financing is usually the better choice.

Expert Tip 💡

Instead of comparing only monthly payments, calculate the total amount you’ll spend over the entire agreement. A lease that seems cheaper today may cost more over several vehicle cycles, while financing can provide years of payment free ownership once the loan is paid off.

Conclusion

The lease or finance decision ultimately comes down to what matters most to you.

If you prefer lower monthly payments, newer vehicles, and regular upgrades, leasing can be an attractive option. It offers flexibility and often provides access to the latest technology without the commitment of ownership.

On the other hand, financing is usually the better choice for people who want long term value, unlimited mileage, and the satisfaction of owning their vehicle. While monthly payments may be higher, those payments eventually end, leaving you with an asset you can continue driving or sell later.

Neither option is universally better. The right choice depends on your budget, driving habits, lifestyle, and long term goals.

Before signing any agreement, review the total costs, mileage limits, fees, and ownership implications carefully. When you match the financing method to your personal needs, you’ll make a decision that feels right both today and years down the road.

Financial Disclaimer

This article is for informational purposes only and should not be considered financial advice. Vehicle lease terms, financing rates, fees, and incentives vary by lender, dealership, and market conditions. Consider consulting a qualified financial professional before making major financial decisions.

I’m Veronica Roth, an author at GrammarGuides.com, where I make English easy to understand. As a grammar expert, I help readers master spelling, punctuation, and common language mistakes.